Profit and loss formula for business owners, including taking a look at an Excel template; plus a pdf download

This article is about profit and loss formula. If you are a business owner who doesn’t really understand the various profit and loss formula, this article should help.

This article is about profit and loss formula. If you are a business owner who doesn’t really understand the various profit and loss formula, this article should help.

Or if you are an entrepreneur who is looking for a bit of clarification on some of the terminology around profit and loss statements, then this article is for you too.

Main sections of this article on profit and loss formular:

- Profit and loss definition

- Summary trading and profit and loss account showing the gross profit only

- What is accrual basis of accounting?

- Definition of profit

- Gross profit definition

- Definition of loss

- Profit and loss formula explained

- Gross profit calculator – Profit and loss worksheet

- Net profit formula

- Net profit calculator – Profit and loss worksheet

- EBITDA margin formula

- Profit and loss problems

- Free Profit margin calculator in Excel and pdf of this article to download

Reason for an article on profit and loss formula

The reason for my article on profit and loss formulas and a review of the profit and loss statement are fourfold:

- My background is in accounting and I have run and owned many businesses. So I know the importance behind understanding a profit and loss account.

- The profit and loss statement for small business can confuse some business owners, so I wanted to help resolve the confusion

- I wanted to provide an easy to use profit and loss template for entrepreneurs to use for free

- I have created a free profit margin calculator in Excel to download to help with the understanding of a profit and loss statement and the profit and loss formulas that go with it.

Profit and loss definition

Before I go into a bit more detail, I feel a profit and loss definition wouldn’t go a miss in this article.

A profit and loss statement or a profit and loss account is a company’s financial statement which summarises income (or revenue) received or earned by the business and costs and expenses incurred whilst creating that same income.

This is an important principle in establishing the profit and loss definition, i.e. the matching principle.

What is the matching principle?

With even the very basic profit and loss statement, a business must usually adopt the matching concept. The matching concept in accounting terms is whereby sales or income generated by a business is match against specific costs incurred whilst generating that same income.

The matching principle is best explained by way of an example:

- Elite Car Sales company sells cars

- The business sells each car at $20,000

- Elite Car Sales purchases the cars for $12,000 each

- At the beginning of the period Elite Car Sales had 5 cars in stock

- During their second year of trading to 30th June 2017 the business purchased 30 cars

- During the same startup year to 30 June 2017 the business sold 24 cars

- At 30 June 2017 Elite Car Sales had 11 cars in stock

Summary trading and profit and loss account showing the gross profit only…

[table id=1 /]

In the above profit and loss account we can see that we matched the correct number of car purchases with the same number of sales.

This ends up with a gross profit of $192,000, which is equivalent to 24 cars at a gross profit of $8,000 per car (or $20,000 – $12,000 = $8,000).

This is an important aspect to the matching principle. To explain this to the extreme, if Elite Car Sales purchased a further 20 vehicles on 30 June 2017, but didn’t include these in closing stock, the business would have made a loss.

Purchases would increase to $500,000 (i.e. $360,000 + (20 x $12,000) or $240,000). So the gross profit above, less the additional $240,000 would change the gross profit into a gross loss of $48,000.

This is clearly wrong accounting and the gross loss would clearly be an error.

In addition to matching the costs or purchases that are directly related to the volume of sales, as demonstrated in the above example, business expenses also need to be accounted for in a similar way. Expenses need to be accounted for on an accrual basis of accounting.

Related: Solvency Ratio Formula – Understanding Solvency Ratios

What is accrual basis of accounting?

Accrual based accounting means that you accrue costs at the end of a period to match the period of account. Again, this is better explained by way of an example:

Accrual basis of accounting example using Elite Car Sales business…

- Rent for the Elite Car Sales showroom is $3,000 per quarter

- Utility costs for the building for the period to 31 December 2017 amounted to $3,000 (In the period to December 2016, the utility cost was $2,800)

- Monthly wages costs amounted to $5,000 per month

- Sales commissions for the sales staff amounted to $2,000 per month for July 2016 through to June 2017, but the $2,000 for July 2016 related to car sales in June 2016. Also, Commission for June 2017 amounted to $2,500, but was paid in July 2017

- Telephone and mobile charges were $500 per month.

- Other business expenses amounted to $1,500 per month.

- Depreciation and amortisation was $5,000

- Interest on bank loan was $6,500

- Tax amounted to $12,000

[table id=2 /]

Now that we’ve taken a look at the definition of profit and loss. We’ve reviewed this using both a trading and profit and loss account and by looking at the matching principle. So let’s define profit, before we begin to look at profit and loss formula.

Definition of profit and what is the formula for profit?

What is the formula for profit?

Many people ask the question ‘what is the formula for profit?’ This question could be taken and answered in one of two ways:

- What is the formula for profit? Meaning; how do I run my business in order to make a profit?

- What is the formula for profit? Meaning; how do you calculate profit margins; like net profit margin and gross profit margin?

Taking each of these questions in turn…

How do I run my business in order to make a profit?

If you are asking the question ‘What is the formula for profit?’ and your reason for asking this question is more about how to run your business in such a way as to make a profit, this article is not about this per se, but it is more about profit and loss formula and how to calculate these.

Having said that, there are many ways you can improve how you run your business to make a profit or increase your profits. Certainly there are many things you can do to improve what you do in order to make a profit.

To begin with, it helps if the business you are running is something you are passionate about. The reason for this is that by having a passion will give you the focus to do whatever it takes to make the business a success.

If you are already making a profit and you are looking to increase your profits, I’ve written a very easy to use program. This program is ‘Increase Profit Software’ and looks at the seven ways to grow your business. For more information on this, please visit my Bowraven website and go to my Increase Profit Software program.

How do you calculate the profit margins like net profit margin and gross profit margins?

Before looking at profit margins, I want to look at a two important definitions…

Net profit definition…

The definition of net profit is the profit that remains after taking cost of sales, all operating costs, interest costs, depreciation and amortisation, taxation and dividends away from sales. Net profit would also include interest income and other income like rent etc. What I’ve just defined is the net profit after tax.

Net profit is also referred to as the ‘Bottom Line,’ or net income or net earnings. The simple formula for net profit is Total Revenue – Total Expenses = Net Profit.

Net profit is the last line on the profit and loss account and is what is most commonly used as the metric for how well a business is performing or not.

When we define profit we are looking at a business which has a surplus remaining after total costs and expenses are deducted from total revenue. The surplus or profit is the amount on which tax is calculated and from which dividends are paid.

In Table 1. above this was illustrated using Elite Car Sales and the net profit before tax in this example was $57,100. The after tax profit is $45,100.

Profit is the life-blood of business. A profitable business will be able to invest in future operations and remain in business for the benefit of the shareholders. Profit tends to be a comparable indicator of business performance. It is also used in calculating the value of a business using a multiple suitable for the type, size and age (or maturity) of the business.

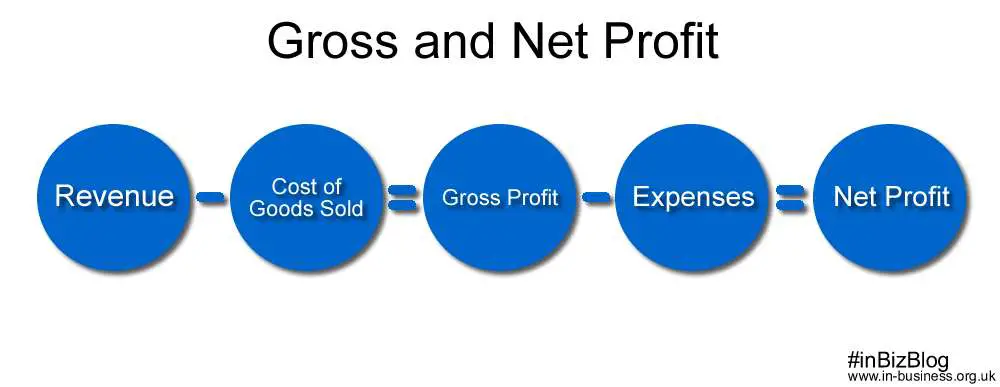

It is however important to distinguish between gross profit and net profit. But generally, when entrepreneurs speak about business profit, they are normally referring to net profit and not gross profit. However, let’s also define gross profit too.

Gross profit definition…

Gross profit is defined as a company’s total revenue (equivalent to total sales) less the cost of goods sold. Another term for gross profit is gross margin, which has been illustrated in Table 1 above. In the example the business sold 24 cars for $480,000. The gross profit was the amount associated with the margin made on the sale of each vehicle, i.e. $8,000 x 24 = $192,000.

Additionally, gross profit is the profit a manufacturing company makes by taking its total revenue then deducting the costs associated with making its products. This calculation gets a little bit more involved and can be more complicated, but the principles are exactly the same.

However, instead of having a simple buying-price of the end product, as we saw in Elite Car Sales, a manufacturing company will usually have a number of associated product costs. So in the case of a car manufacturer, the raw material costs will include steel or aluminium for the car’s body, glass for the windows, tyres for the wheels, etc. The amalgamation of all these costs will make up cost of goods sold, after adjusting for opening and closing stock of each raw material.

Finally, for a service type business gross profit is total revenue less the costs associated with providing its services.

Definition of loss and how do you calculate a loss?

When we define loss we are now looking at the amount of money that an organisation loses in a period instead of a profit.

So a loss is where total costs and expenses exceed total revenue. This is most common in the startup year(s) of a business, but can also happen during a recession or if a new competitor sets up and ‘steals’ your customers.

A simple formula to calculate a loss is: Total Revenue – Total Expenses = Net Loss

A business will need to have sufficient working capital to trade through a loss making period to avoid liquidity problems. However, in most countries around the world, where a business sustains a loss, no tax will be due. Also, the loss can usually be used to be set against future business trading profits too.

For startup businesses the need to have sufficient opening investment funds (or working capital) to be able to trade through opening losses is vital. Bearing in mind 8 out of 10 small businesses fail within their first 12 months, and of the 2 that survive 50% of those do not survive the next two years.

Related: Symptoms of Overtrading

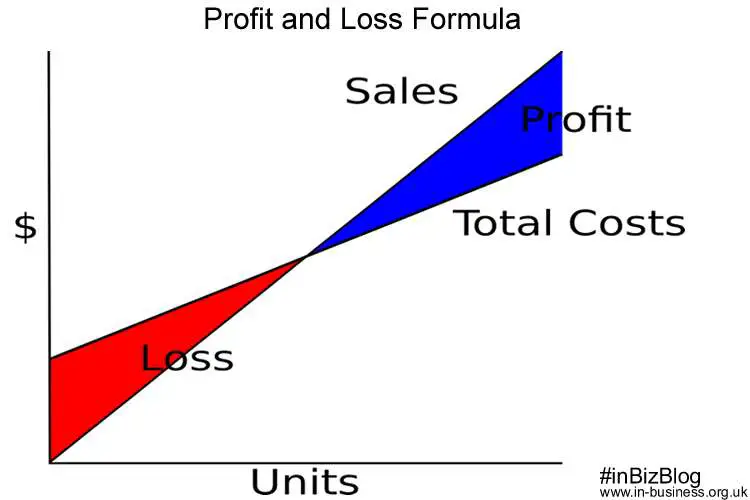

Profit and loss formula explained…

So now that we have defined a profit and loss and also looked at the definition of net profit and gross profit together with a loss, we can now look at profit and loss formula in more detail.

So now that we have defined a profit and loss and also looked at the definition of net profit and gross profit together with a loss, we can now look at profit and loss formula in more detail.

The profit and loss formula we are going to review are:

- Gross profit formula

- Net profit formula

- EBITDA margin formula

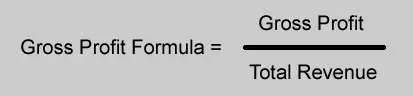

Gross profit formula or gross profit margin formula…

The gross profit margin formula is calculated by subtracting the cost of goods sold (COGS) from total revenue and then dividing that number by total revenue.

In the Excel template below I have created a gross profit calculator or gross margin calculator. The numbers used in the uploaded Excel example are from the Elite Car Sales Company above. You can download the calculator for free and use it with your own numbers.

The gross profit margin formula for calculating the gross profit margin is as follows:

Gross profit percentage = Gross Profit (Total Revenue – Cost of Goods Sold)/Total RevenueWith the example the gross profit percentage = $192,000/$480,000 = 40%

Gross profit calculator and profit and loss worksheet…

To do your own gross margin calculation I have provide you with a profit and loss worksheet. Click on the download link below the viewing window to download the free gross profit calculator.

[embeddoc url=”https://www.in-business.org.uk/wp-content/uploads/2017/08/Gross-profit-calculator.xlsx” download=”all” viewer=”microsoft”]

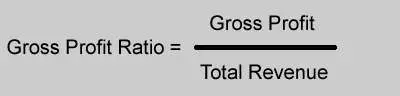

What is gross profit ratio?

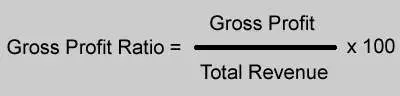

Another way to describe gross profit margin is gross profit ratio. The reason some use ratio instead of margin is because the formula is the ratio between gross profit and sales. So in the same way of calculating profit margin or gross profit margin, gross profit ratio is calculated as follows:

And expressed as a percentage – gross profit ratio percentage or gross profit percentage formula:

Now that the gross profit formula has been explained in detail, the next profit and loss formula to review is the net profit formula…

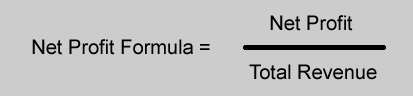

Net profit formula

The formula for net profit is to take the gross profit and subtract the expenses of the business. In the example of Elite Car Sales total expenses amounted to $134,900. With a gross profit of $192,000, the net profit calculation (before tax) for this business is $192,000 – $134,900 = $57,100.

Now having the calculation of net profit, next is the net profit formula. Other terms are net profit ratio or net margin formula. These are calculated as follows:

In the case of Elite Car Sales the net profit formula to calculate the net profit percentage is: $57,100/$480,000 = 11.9%.

Net profit calculator and profit and loss worksheet…

Like the gross profit calculator above, I have provided another profit and loss worksheet. This one is a net profit calculator to help you calculate net profit.

To do your own net profit calculation click on the download link below the viewing window to download the free net profit calculator.

[embeddoc url=”https://www.in-business.org.uk/wp-content/uploads/2017/08/Net-profit-calculator.xlsx” download=”all” viewer=”microsoft”]

What is operating profit or EBIT?

Another expression to review is operating profit and the associated operating profit formula. Operating profit, also referred to as EBIT is the profit a business earns from its ‘normal’ core operations.

So any income received by a business from investments it holds, like interest or rental income, is excluded from operating profit.

Also, operating profit is before the deduction of interest on loans or overdrafts and taxation too. Using operating profit or EBIT is a useful tool for investors to compare businesses across an industry.

By ‘stripping-out’ the costs associated with debt obligations and income associated with investments, the comparable profit is easier to review.

It is possible for a business to make an operating profit but overall still make a loss. This would be the result of a heavily debt laden company, where the costs associated with borrowings are taking the business into a loss making situation.

So operating profit is calculated as:

Operating profit = Operating Revenue (total sales) – COGS – Operating Expenses – Depreciation & Amortisation

The business operating margin formula is Operating profit/Total Revenue, which is shown in the free Excel net profit calculator. In the case of Elite Car Sales the operating profit ratio or margin is $63,600/$480,000 = 13.25%.

Other profit formulas including EBITDA margin formula…

In addition to net profit formula and operating or EBIT profit margin calculations there are other profit and loss formula to review. One of these further formulas is EBITDA margin formula.

What is EBITDA?

EBITDA is often referred to by investors, entrepreneur and accountants when talking about business profits. The term EBITDA stands for Earnings Before Interest, Tax, Depreciation and Amortisation.

Investors use EBITDA to analyse and compare profitability between companies and industries. This formula eliminates the effects of financing and accounting decisions.

How to calculate EBITDA is better explained by way of an example. So using the Elite Car Sales company example:

[table id=3 /]

Table 3 shows the EBITDA calculation. If you want to learning how to calculate EBITDA using MS Excel – please download the net profit calculator above.

Many times EBITDA is the profit used in business valuations.

Net profit after tax and the profit after tax formula…

Net profit after tax is simply the net profit of the business after deducting the tax charge. The tax charge will be calculated using the net profit figure. In most countries the net profit will be adjusted for non-taxable expenses.

In the example of Elite Car Sales the net profit after tax is $45,100. So the profit after tax formula to calculate net profit after tax ratio or percentage = $45,100/$480,000 = 9.3%

Net profit before tax and the profit before tax formula…

The term profit before tax is synonymous with net profit. So the profit before tax formula to calculate profit before tax percentage = $57,100/$480,000 = 11.9%.

Gross and net profit…

Now that you have an understanding or gross and net profit, you will be better placed to understand the numbers in your business. Each number has a use in understanding how the business is doing.

The importance of gross profit and gross profit formula…

For example, it’s important to understand the importance of making a gross profit. A business that makes a gross loss might as well pack up and go home right away. However, once you understand gross profit and gross profit margins, it becomes even more important to drill down into individual product or service gross profits and gross profit margins.

Each product or service in any business should make a gross profit. If not, either stop selling that product or service, or increase the selling price. This of course assumes that the market can take a price increase.

The only time where a gross loss on a particular product or service is acceptable for a business is using it as a loss-leader. A loss leader is where a product is given away for free or at a loss in order to gain further sales of profit-making products from the same customer. It’s where the term “A sprat to catch a mackerel comes from”.

The importance of net profit and net profit formula…

Net profit and net profit formula are important business key performance indicators (KPIs). Net profit for a business is a health indicator. The more profitable a business becomes, the better the business is in the eyes of investors and the more valuable it becomes.

Profit is a value-metric used to value businesses of all sizes. However, the profit used in business valuation does vary. Sometimes this will be net profit, but as already discussed this is more likely to be EBITDA.

Knowing your business net profit and net profit margins will allow you to monitor how well the business is doing from one year to the next. You can also begin to target profit improvement techniques, like reviewing the average transaction value.

Implementing profit improvement techniques, whilst monitoring profit and loss formulas will allow you to know whether the implemented techniques are working or not, and by how much.

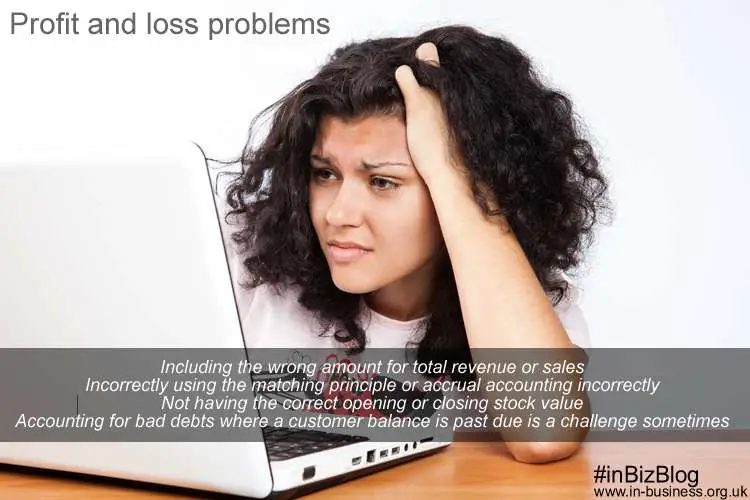

Profit and loss problems

Profit and loss problems would include the following examples:

Profit and loss problems would include the following examples:

- Including the wrong amount for total revenue or sales

- Incorrectly using the matching principle or accrual accounting incorrectly

- Not having the correct opening or closing stock value

- Accounting for bad debts where a customer balance is past due is a challenge sometimes

Including the wrong amount for total revenue or sales…

When including total revenue on the profit and loss account it is important to include the correct sales figures. For example, where a business accounts for Sales Tax or VAT, the sales included on the profit and loss account should be net of Sales Tax or VAT.

Also, any discounts given to customers for early payment or bulk purchases discounts should be netted against sales.

Another profit and loss problem is in which accounting period to account for a sale. This may seem obvious, but not always. For example, sales invoices at or around the year end may not be raised until the new accounting period. The work has been done or the products have been shipped, but the invoices are not dated in the same period as when the sale took place.

In this example, the value associate with these ‘late-raised-invoices’ should be accrued back into the financial period to which they relate.

Incorrectly using the matching principle or accrual accounting incorrectly…

Not using the matching principle or accrual account correctly is easily done by an inexperienced bookkeeper or accountant. Or where a new business owner is preparing his own accounts, they may not understand the matching principle.

It is easy to simply include costs and expenses that have been paid for in the accounting period. Whereas, as already shown in the above Elite Car Sales example, expenses not only straddle accounting periods, but bills for expenses incurred in the period can be received late.

It is therefore important to review bills received in the immediately following accounting period. Any bills which relate to the prior period should be accrued and adjusted for accordingly.

Not having the correct opening or closing stock value…

In the above profit and loss statement example with Elite Car Sales, I reviewed cost of goods sold taking account of stock. This is something that can cause profit and loss problems. One such problem is where a stock count is not made at the year end. All businesses which carry stock must carry out a stock check. This must be done on the year end date (or as close as possible to that date)

In order to get an accurate cost of goods sold figure, and therefore the correct gross profit and net profit, stock needs to be correctly accounted for.

Another problem for accounting for the correct profit or loss, is how to treat obsolete stock, and when to write it off. At the stock check, if obsolete stock is counted and included in closing stock, the profit will be overstated on the profit and loss statement.

Accounting for bad debts where a customer balance is past due is a challenge sometimes…

At the final closing of the financial statements, a final review of the balance sheet should be done. In particular a review of the trade debtors should be done. Where a customer is not paying inline within your payment terms, and especially where the debt is getting old, a potential bad debt provision needs to be made.

Understanding this concept and making a decision as to whether to provide or not does cause problems when trying to arrive at an accurate profit or loss.

Profit and loss statement for self employed

The profit and loss statement for self employed businesses does not need to follow strict disclosure requirements. However, the way of recording the data remains the same as it is for a small business trading as a limited company. All the concepts I have already discussed, like the matching principle and the accruals concept apply.

Making sure that sales are disclosed net of trade discounts and Sales Tax or VAT also applies.

The net profit and gross profit principles apply the same for self employed profit and loss statements too. The method used to calculate the various profit and loss formula remains the same.

Profit and loss statement for small business

Unlike the profit and loss statement for the self employed, the profit and loss statement for small business must follow certain disclosure guidelines. However, apart from this, the principles for a small business are the same, where the net profit and gross profit calculations are the same. The profit and loss formula calculations are all the same too.

Year to date profit and loss statement versus current month profit and loss account

Most organised businesses track their month-by-month profit and loss accounts. This will allow them to review both current month profit and loss and the year to date profit and loss on a regular basis.

Businesses which prepare an annual business plans and budgets will not only compare the monthly profit and loss numbers to the budget, but also the year to date profit and loss statement too.

In addition to comparing both these profit and loss statements to budgets, they also need to be compared to the previous year figures. This will provide a good metric for business management. Using the comparable data they’ll know whether the business is doing better or worse each month and so far year to date.

Where a business prepares monthly profit and loss accounts, a month end stock check also needs to be performed. This ensures that the management accounts reflect an accurate profit or loss for the period, and for the year to date.

Profit and loss questions

If you have any profit and loss questions please feel free to contact me. Alternatively, post your questions below in the comments. It would be better to post these in the comments, because others will benefit from the answers to your question.

Free Profit margin calculator in Excel to download…

To download both profit margin calculators please click on the relevant link below. Also, you can download this article in pdf format too:

Profit and loss formula pdf download

Finally please social share and comment below…

If you enjoyed reading this article about profit and loss formula, please share. Choose your favourite social media channel below. I’d also appreciate your comments below too, and thank you for reading in-Business Blog.

Related: How to Calculate Net Worth

With even the very basic profit and loss statement, a business must usually adopt the matching concept. The matching concept in accounting terms is whereby sales or income generated by a business is match against specific costs incurred whilst generating that same income.